Retirement lifestyle is all about choices. Do you wish to refinance your home to create monthly income or is it time to downsize and buy a condo? Maybe you just need a standby line of credit to serve as a safety fund? Whichever you need, it could be time to look at a Reverse Mortgage.

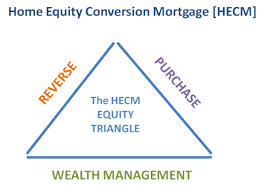

Each of these options is part of the three primary components of the Home Equity Conversion Mortgage (HECM), commonly referred to as the Reverse Mortgage lending program insured by FHA and managed by HUD. And each is designed to offer a unique solution to a specific financial challenge faced by those persons at least age 62.

In the simplest of terms, the Reverse Mortgage can be viewed as a basic cash-out refinance with deferred payments. That is, if you own a home with an existing loan balance, and assuming that there is sufficient home value and available equity, the HECM Lender may refinance your existing mortgage and enable you to live in your home without any requirements to make a monthly mortgage payment. Additional funds available beyond those required to pay off any existing mortgages and liens may be distributed as desired, either as regular monthly deposits to your checking account, or as lump-sum distributions, or a combination thereof. Real Estate Taxes and Homeowners Insurance still must be paid by the homeowner. The loan balance becomes due when the borrowers decide to sell or move away, or at the time that the last remaining borrower passes away.

The second option is to use the HECM Program to downsize to a new home. Many seniors will sell a prior home and, because they cannot or are unwilling to qualify for a new mortgage on the new home, they will go to the closing table with an all cash transaction. Consider the fact that the borrower in this scenario has just extracted all the prior equity out of the ground and is now willingly plowing those funds back into the ground again. This action may not be a wise use of funds for any retiree, mainly because available cash is a major consideration for managing retirement finances. Suppose, instead, that the buyers choose the HECM for Purchase Program (H4P). In this scenario, depending on the age of the youngest borrower, the buyers could use a smaller amount of actual cash to fund the down-payment and simply borrow the difference under the H4P Program. The result is that the buyers get to keep much of their recently extracted equity for financial security and can simultaneously enter into a HECM mortgage with terms that would not require any monthly mortgage payments.

The third option is specifically designed to address a Wealth Management scenario. If you have an investment portfolio and systematically sell portions of your portfolio to extract income, regardless of market conditions, you are at risk of losing past and future gains when selling in a down market. The solution is to initiate a HECM Line of Credit to serve as a ready source of financial security in times of stress. And, unlike a standard bank-originated Home Equity Line of Credit, the HECM cannot be cancelled, reduced, modified, or withdrawn regardless of any subsequent reduction in the market value of the home. The HECM Line of Credit can also be a clever way to access funds for charitable gifting. We’ll talk about that in a future story.

Additional insights can be found at www.SeniorLifestyle Mortgage.com

William R. Hornbeck, Principal SeniorLifestyleMortgage.com

NMLS# 1221314 Your Source for HECM Insights and Knowledge