A new Congressional Budget Office report projects an even more dire outlook for Social Security’s future than was previously calculated. Without action to fix the situation, huge benefit cuts for recipients will begin in 2033. And preventing those cuts will require massive tax increases for working Americans beginning immediately.

In contrast to the Social Security trustees’ own projections, the CBO estimates that Social Security’s combined retirement and disability insurance programs will run out of money two years earlier—2033 instead of 2035—and that the tax increases necessary to fund scheduled benefits are higher than the Social Security trustees projected—4.9 percentage points instead of 3.24.

The divergence comes from different economic and demographic assumptions—of which the CBO’s are significantly more realistic.

For example, the CBO uses a lower fertility rate that is more in line with current trends while the trustees assumed fertility rates will significantly increase. The fertility rate is the total number of births in a year per 1,000 women of reproductive age.

The trustees also assumed only 4.5% price inflation in 2022 and 2.3% in 2023 while the CBO report accounted for the recent 8.7% cost-of-living increase for 2023.

Under either set of projections, Social Security’s future is not secure. The program is running out of time and money, recent increases in government spending and debt have crowded out options for reform, and virtually all Americans stand to lose from policymakers’ inaction.

Americans deserve to know the truth about Social Security’s future so that they can assess the best options for reform. The CBO report reveals five hard truths:

- Social Security has a spending problem. Social Security started out as a 2% tax, and the program promised to never take more than 6% of workers’ paychecks. Today, it takes 12.4%, and even that falls far short of the program’s ever-rising costs. The CBO projects that Social Security’s costs will increase by 42% over the next 75 years as its revenues remain stable. Protecting Social Security requires reining in its excessive cost growth.

- Inaction means benefit cuts of 23% beginning in 2033. Current law requires that Social Security benefits come from within the program, so once the trust fund runs dry, Social Security will only be able to pay as much in benefits as it receives in taxes. That will mean a roughly $5,000 cut in annual benefits for a typical retiree and about $4,000 less for the average disability beneficiary. No one—not even 98-year-olds—will be exempt from these cuts.

- Anyone who is 56 years old or younger today won’t receive a full benefit. Anyone who is 56 or younger today will not reach Social Security’s normal retirement age of 67 before the program runs out of money. And anyone who is currently between the ages of 57 and 107 today who is still alive and collecting benefits in 2033 will also be subject to benefit cuts.

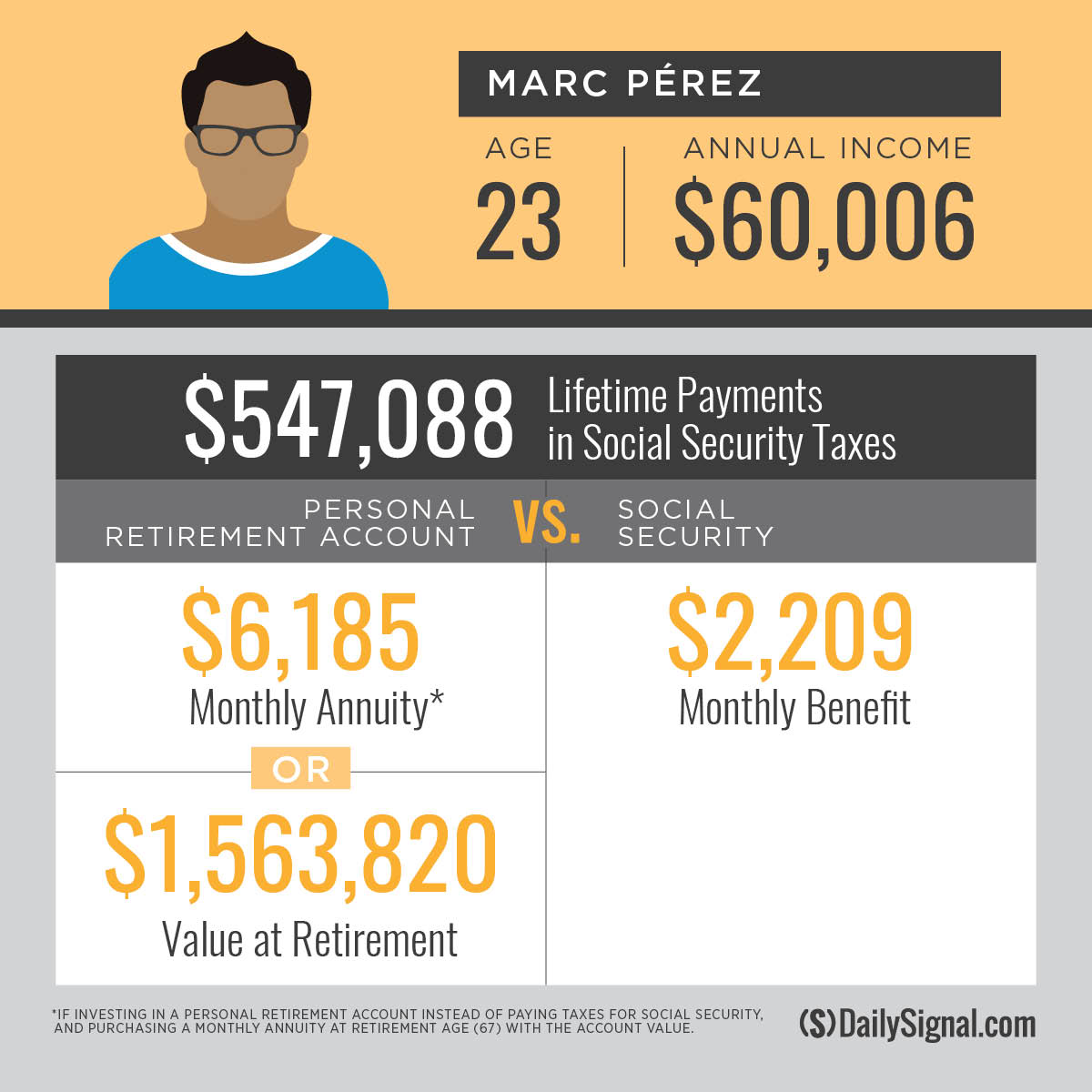

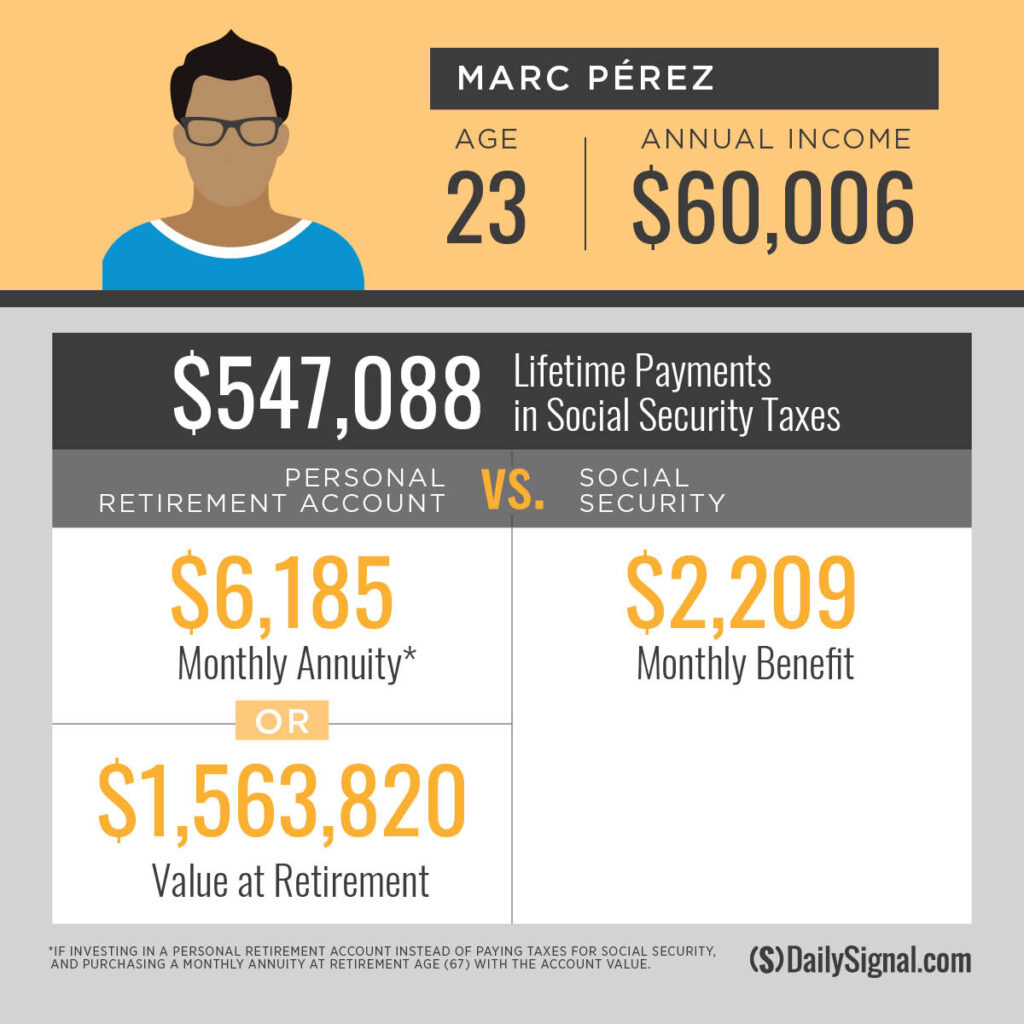

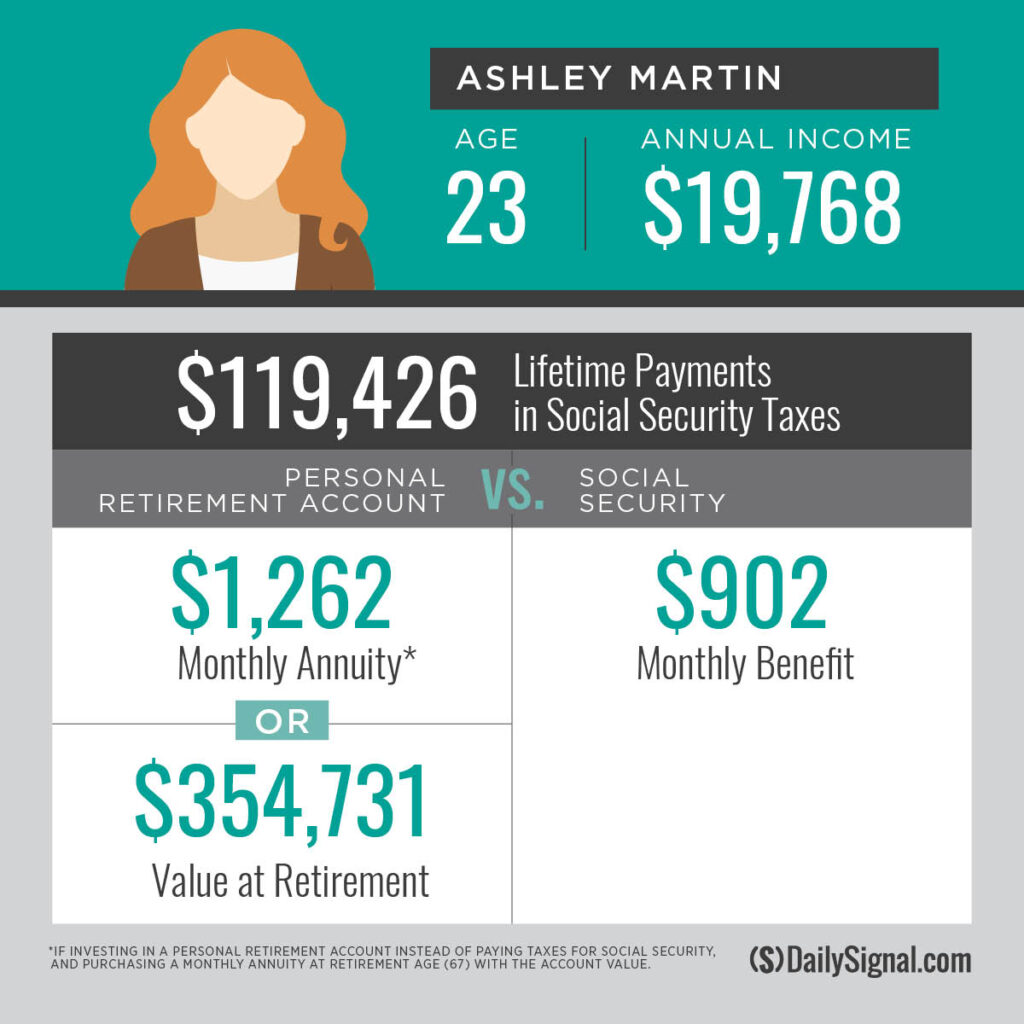

- Younger workers have the most to lose. If policymakers fail to act and benefit cuts begin in 2033, the CBO estimates that people born in the 1960s will experience a 19% reduction in their lifetime benefits, those born in the 1970s will experience a 26% reduction, and those born in the 1980s and 1990s will experience a 27% reduction. Research from The Heritage Foundation shows that Social Security is an especially raw deal for younger workers who have to put their money into a broken system instead of into savings accounts that would generate positive returns. The average worker could have three times as much retirement income if they had been able to own and invest their Social Security taxes—and even the lowest-income workers could have 40% more. See the two examples below.

- Preventing insolvency through tax increases would require a 17.3% payroll tax. The CBO says that maintaining Social Security’s scheduled benefits for the next 75 years would require an immediate increase in Social Security’s payroll tax, from 12.4% to 17.3%. This would mean $12,250 in Social Security taxes for the median household that has about $71,000 of income. Adding in Medicare and federal and state income taxes would bring the median household’s marginal tax rate to about 48%.

The CBO report reveals a bleak future for the majority of Americans who have been forced to pay into Social Security’s broken system.

While there’s no way to undo past excesses that have made Social Security both popular and bankrupt, the good news is that there’s a way to protect the most vulnerable Americans while improving Social Security for current and future generations. Heritage’s Budget Blueprint provides an entire plan of reforms.

For years, politicians have turned a blind eye to Social Security’s insolvency—even as its deficits have surged to $20.4 trillion, or $157,000 per household. But policymakers should embrace Social Security reform as a way to benefit all Americans.

By focusing the program on its purpose of providing financial security and protecting seniors from poverty, modernizing the program to today’s economy and labor market, and allowing workers the option of using part of their Social Security taxes to build wealth in personal accounts that they own, it’s possible to make more people—and the entire economy—better off.

Rachel Greszler is a research fellow in economics, budget, and entitlements in the Grover M. Hermann Center for the Federal Budget, of the Institute for Economic Freedom, at The Heritage Foundation. Reproduced with permission. Original here.