There’s an odd sense of fear going around the financial world. It’s almost as though no one can believe that the Dow Jones record-breaking streak is real. People are looking for bubbles to burst everywhere. Sub-prime loans are back. Student debt is over $1.3 TRILLION. Now is the time to ask how safe is your bank account if there’s a run on it.

Make sure your that bank is insured (some aren’t) by asking the branch manager or looking for the FDIC logo. Then, check if your money is within the FDIC limit. You can visit the FDIC’s Electronic Deposit Insurance Estimator to help you determine this.

According to the FIDC website: Your bank accounts are covered by FDIC insurance. That’s now up to $250,000 per account. FDIC insurance does not cover other financial products and services that banks may offer, such as stocks, bonds, mutual funds, life insurance policies, annuities or securities. The standard insurance amount is $250,000 per depositor, per insured bank, for each account ownership category.

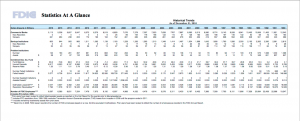

However, the FDIC itself is grossly undercapitalized at just a 1.2% reserve ratio (see image) so if there was a massive run on banks – a catastrophic banking system failure – the government would have to print money to repay all the insured victims which would trigger a massive wave of inflation. And even assuming FDIC coverage protects your deposits from bank failures, it doesn’t protect you from most other threats to your account.

Remember, FDIC insurance provides no coverage for brokerage accounts, insurance policies, and other non-bank financial accounts and no protection against identity theft. You might be able to recover funds taken fraudulently from your accounts. Unless you have ID theft insurance, you’ll be responsible for restoring your accounts and your credit history and any costs that involves.

Remember, FDIC insurance provides no coverage for brokerage accounts, insurance policies, and other non-bank financial accounts and no protection against identity theft. You might be able to recover funds taken fraudulently from your accounts. Unless you have ID theft insurance, you’ll be responsible for restoring your accounts and your credit history and any costs that involves.

Insuring the Federal Deposit Insurance Corporation

According to the FDIC, no one has ever lost a single penny of insured deposits in its 75-year history. This is good to know, but with so many failed banks in 2008 alone, many people are still skeptical. (From Investopedia.)

The FDIC stated publicly in September of 2008 that it did not anticipate that there would be enough bank failures to deplete the $52 billion Deposit Insurance Fund (DIF). This fund, composed of the premiums banks pay to have their deposits insured, is controlled by the FDIC. If the DIF were to be depleted, the FDIC also has a $30 billion line of credit with the Department of Treasury and the federal government’s guarantee that if the FDIC exhausts its other options, the government will step in to provide further financial backing.

In addition, FDIC insurance provides no protection from judgment creditors or the IRS. The government can levy your accounts for unpaid taxes. And, FDIC insurance won’t stop your money from being stolen by state governments under Dormant Funds laws.

Dormant accounts may be stolen by the government.

If you don’t use your bank account for a year, your bank may flag it as dormant. They may approach you to see whether it’s still in use, but if you don’t reply, after a period of time varying from one to seven years depending upon bank and state, your dormant account will be turned over to the state government – who are always on the look-out for free money.

To locate any funds that may have been seized due to extended dormancy, visit the website of your local state comptroller. Many states have online search options that require only your first and last name to discover what monies you may have neglected to collect over the years. Some states prefer to let an outside agency handle the details, but in either case you will be directed to the right place for performing a search. Once you’ve found unclaimed assets that belong to you, a claim can be made electronically or by mail.

The message is to keep on top of your record keeping. Monitor all of your accounts and assets carefully. Keep bank accounts “alive” by using them at least once a year. Keep a very accurate record of all your accounts in a place where your heirs can find it.

And share this information with family members. Think about old or sick parents or siblings. Have they been able to access all their bank accounts in a while? Is there an estate account with unclaimed money? Don’t let the government just take your money!