Once upon a time the Fed made profits and sent those profits to the US Treasury. It was usually billions of dollars per year.

Now because of reverse repos* and interest paid on reserves to commercial banks, the Fed is paying approximately $700 million PER DAY to commercial banks to keep the system from falling apart.

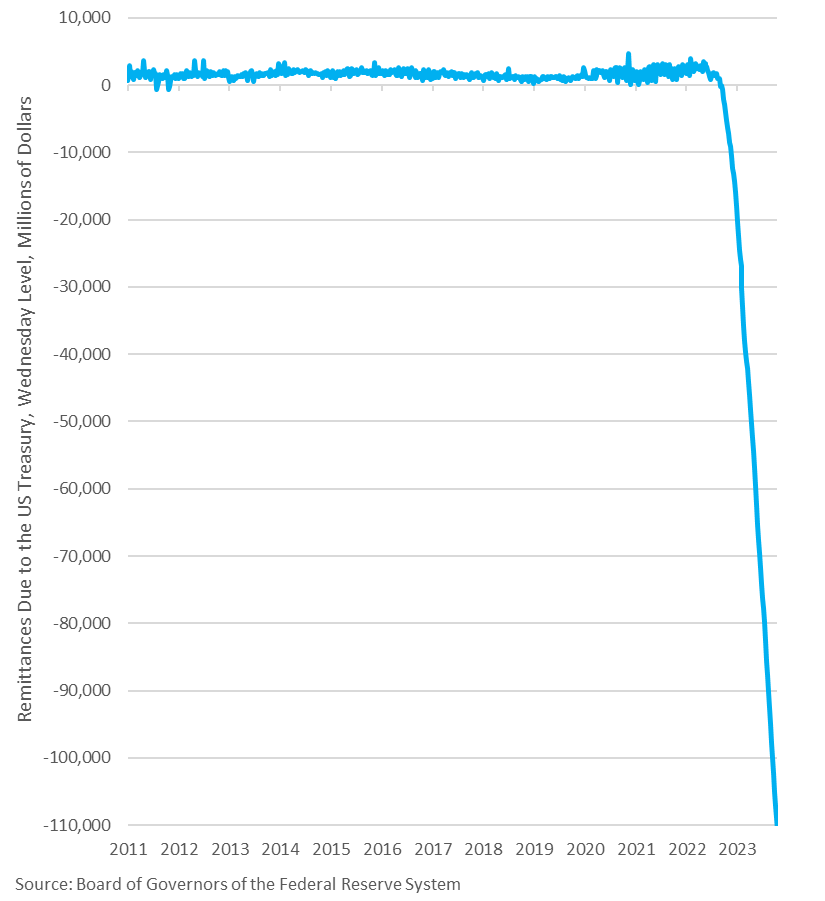

We're gonna need a bigger graph: Fed is now over $110 billion in the hole after suffering another week of losses in an unprecedented streak or red ink – the same people telling you the banking system is safe and sound found a way to lose money despite having a money printer: pic.twitter.com/qCLlVkqVc5

— E.J. Antoni, Ph.D. (@RealEJAntoni) October 20, 2023

US paid $853 Billion in Interest for $31 Trillion Debt in 2022; More than Defense Budget in 2023.

— Wall Street Silver (@WallStreetSilv) January 27, 2023

If the Fed keeps rates at at these levels (or higher) we will be at $1.2 trillion to $1.5 trillion in interest paid on the debt.

The US govt collects about $4.9 trillion in taxes. pic.twitter.com/L0TQDWMhi6

*Repo vs. Reverse Repo: An Overview

The repurchase agreement (repo or RP) and the reverse repo agreement (RRP) are two key tools used by many large financial institutions, banks, and some businesses. These short-term agreements provide temporary lending opportunities that help to fund ongoing operations. The Federal Reserve also uses the repo and RRP as a method to control the money supply.1

Essentially, repos and reverse repos are two sides of the same coin—or rather, transaction—reflecting the role of each party. A repo is an agreement between parties where the buyer agrees to temporarily purchase a basket or group of securities for a specified period. The buyer agrees to sell those same assets back to the original owner at a slightly higher price.

Both the repurchase and reverse repurchase portions of the contract are determined and agreed upon at the outset of the deal.

KEY TAKEAWAYS

- Repurchase agreements, or repos, are a form of short-term borrowing used in the money markets, which involve the purchase of securities with the agreement to sell them back at a specific date, usually for a higher price.

- Repos and reverse repos represent the same transaction but are titled differently depending on which side of the transaction you’re on. For the party originally selling the security (and agreeing to repurchase it in the future), it is a reverse repurchase agreement (RRP). For the party originally buying the security (and agreeing to sell in the future) it is a repurchase agreement (RP) or repo agreement.

- The repurchase agreement involves the purchase of an asset that is held as collateral until it is resold to the counter-party at a premium.

Repo

A repurchase agreement (RP) is a short-term loan where both parties agree to the sale and future repurchase of assets within a specified contract period. The seller sells a security with a promise to buy it back at a specific date and at a price that includes an interest payment.

Repurchase agreements are typically short-term transactions, often literally overnight. However, some contracts are open and have no set maturity date, but the reverse transaction usually occurs within a year.

Dealers who buy repo contracts are generally raising cash for short-term purposes. Managers of hedge funds and other leveraged accounts, insurance companies, and money market mutual funds are among those active in such transactions.

Securing the Repo

The repo is a form of collateralized lending. A basket of securities acts as the underlying collateral for the loan. Legal title to the securities passes from the seller to the buyer and returns to the original owner at the completion of the contract. The collateral most commonly used in this market consists of U.S. Treasury securities. However, any government bonds, agency securities, mortgage-backed securities, corporate bonds, or even equities may be used in a repurchase agreement.

The value of the collateral is generally greater than the purchase price of the securities. The buyer agrees not to sell the collateral unless the seller defaults on its part of the agreement. At the contract-specified date, the seller must repurchase the securities and pay the agreed-upon interest or repo rate.

In some cases, the underlying collateral may lose market value during the period of the repo agreement. The buyer may require the seller to fund a margin account where the difference in price is made up.

How the Fed Uses Repo Agreements

In the U.S., standard and reverse repurchase agreements are the most commonly used instruments of open market operations for the Federal Reserve.1

The central bank can boost the overall money supply by buying Treasury bonds or other government debt instruments from commercial banks. This action infuses the bank with cash and increases its reserves of cash in the short term. The Federal Reserve will later resell the securities back to the banks.

When the Fed wants to tighten the money supply—removing money from the banking system—it sells bonds to the commercial banks using a repo. Later, the central bank will buy back the securities, returning money to the system.2

Disadvantages of Repos

Repo agreements carry a risk profile similar to any securities lending transaction. That is, they are relatively safe transactions as they are collateralized loans, generally using a third party as a custodian.

The real risk of repo transactions is that the marketplace for them has the reputation of sometimes operating on a fast-and-loose basis without much scrutiny of the financial strength of the counterparties involved, so some default risk is inherent.

There is also the risk that the securities involved will depreciate before the maturity date, in which case the lender may lose money on the transaction. This risk of time is why the shortest transactions in repurchases carry the most favorable returns.

A repurchase agreement involves the purchase of securities from a counter-party subject to an agreement to resell the securities back at a later date.

Reverse Repo

A reverse repurchase agreement (RRP) is an act of selling securities with the intention of buying those same assets back in the future at a profit. This process is the opposite side of the coin to the repurchase agreement. To the party selling the security with the agreement to buy it back, it is a reverse repurchase agreement. To the party buying the security and agreeing to sell it back, it is a repurchase agreement.

In a reverse repurchase agreement, a dealer sells securities to a counterparty with the agreement to buy them back at a higher price at a later date. The transaction is completed with a repo agreement. That is, the counterparty will buy the securities back from the dealer as agreed.

While the purpose of the repo is to borrow money, it is not technically a loan: Ownership of the securities involved actually passes back and forth between the parties involved. Nevertheless, these are very short-term transactions with a guarantee of repurchase. As a result, repo and reverse repo agreements are termed as collateralized lending because a group of securities—most frequently U.S. government bonds—acts as collateral for the short-term loan agreement. Thus, on financial statements and balance sheets, repo agreements are generally reported in the debt or deficit column as loans.

What Are Repurchase and Reverse Repurchase Agreements?

Repurchase agreements, or repos, involve the purchase of securities with the agreement to sell them back at a specific date, usually for a higher price. Repos and reverse repos represent opposite sides of the transaction. For the party selling the security and agreeing to repurchase it in the future, it is a reverse repurchase agreement (RRP). For the party buying the security and agreeing to sell in the future, it is a repurchase agreement (RP).

Who Uses Repo Agreements?

Dealers who buy repo contracts are generally raising cash for short-term purposes. Hedge funds, insurance companies, and money market mutual funds may take advantage of repo agreements to receive a short-term infusion of cash. The Federal Reserve and other central banks also use repos to temporarily increase the supply of reserve balances in the banking system.

Is a Repurchase Agreement a Loan?

A repurchase agreement is technically not a loan because it involves transferring ownership of the underlying assets, albeit temporarily. However, since the parties agree to both sides of the transaction (the repo and reverse repo), these transactions are considered as equivalent to collateralized loans and are generally reported as loans on the entities’ financial statements.

The Bottom Line

Repurchase agreement (repo or RP) and reverse repo agreement (RRP) refer to the complementary sides of a transaction that involves the temporary purchase of assets with the agreement to sell them back at a slight premium in the future. For the original seller of the assets who agrees to buy them back in the future, the transaction is a reverse repo. For the original buyer who agrees to sell the assets back, it is a repo transaction. Although treated as a collateralized loan, repurchase agreements technically involve a transfer of ownership of the underlying assets.